India’s real estate sector offers rewarding investment opportunities for Non-Resident Indians (NRIs). However, the legal and procedural hurdles are not to be overlooked. This guide aims to provide a structured roadmap for NRI investment in Indian real estate, simplifying the complexities involved. Stay tuned as we delve deeper into this journey, aiding you in making informed and strategic decisions.

A Non-Resident Indian (NRI) is an Indian citizen who resides outside India for a stipulated period. The definition of an NRI is outlined under the Foreign Exchange Management Act (FEMA) and the Income Tax Act. According to FEMA, an individual is considered an NRI if they stay abroad for employment, carrying on business or vocation outside India, or under circumstances indicating an intention for an uncertain duration of stay abroad.

Other Eligible Entities

Person of Indian Origin (PIO):

A Person of Indian Origin (PIO) is an individual who, or whose ancestors, were Indian nationals but are now citizens of another country, excluding Pakistan, Bangladesh, Sri Lanka, Afghanistan, China, Iran, Nepal, or Bhutan. PIOs have been granted several rights and privileges, including the ability to invest in Indian real estate.

Overseas Citizen of India (OCI):

An Overseas Citizen of India (OCI) is a foreign national who was eligible to become a citizen of India on January 26, 1950, or was a citizen of India at any time thereafter, or belonged to a territory that became part of India after August 15, 1947. OCIs have rights equivalent to NRIs for investment in real estate, with a few exceptions.

Understanding your eligibility status is the preliminary step in the journey of real estate investment in India. It sets the foundation for the subsequent processes, ensuring compliance with the legal and procedural requisites of real estate transactions in India. This clarity is crucial as it delineates the pathway for NRIs, PIOs, and OCIs, aiding in the seamless execution of their investment endeavours.

Financial Planning For NRI Investment in Indian Real Estate

Embarking on a real estate investment journey necessitates a robust financial plan and a well-thought-out budget.

It’s imperative to have a clear understanding of your financial standing, the budget for your investment, and the cost structure involved in real estate transactions.

Here’s a step-by-step approach to ensuring a solid financial foundation for your investment venture.

Assessing Your Financial Health

Before diving into the real estate market, assessing your financial health is crucial. This involves:

Analyzing your savings, income streams, and financial obligations.

Understanding your credit score and its implications on loan eligibility.

Evaluating your risk tolerance and long-term financial goals.

Setting a Budget:

Determining a budget is a pivotal step that guides your investment decisions. Here’s how you can go about it.

Ascertain the amount you can afford to invest without jeopardizing your financial stability.

Account for down payment, home loan EMIs, registration charges, and other related expenses.

Keep a buffer for unforeseen circumstances or cost overruns.

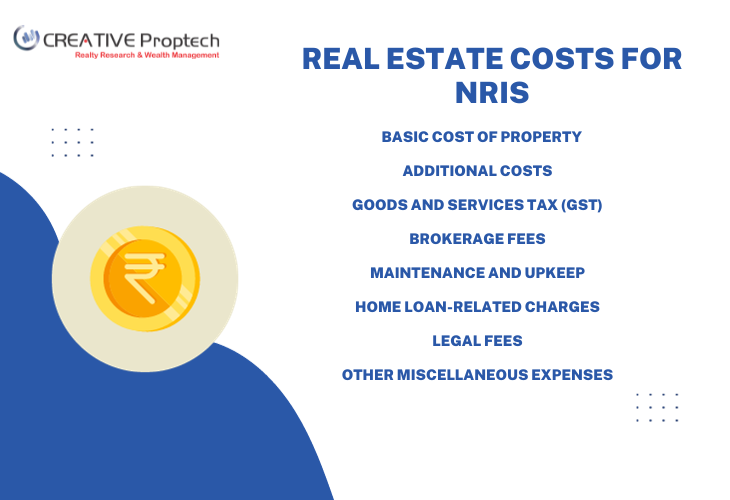

Understanding the Cost Structure in Real Estate Investment

Understanding the cost structure in real estate is akin to navigating through a roadmap. It’s about foreseeing the tolls ahead, ensuring a smooth journey towards a rewarding investment. Each cost, from the basic property price to legal fees, is a milestone on this journey, and having a clear picture helps in making informed decisions.” – Raja Shambhu, Chairman, Creative Proptech

The cost structure in real estate investment goes beyond the price tag of the property. It encompasses:

Basic Cost of Property:

This includes the base price per square foot and other charges like preferential location charges (PLC), floor rise charges, etc.

Additional Costs:

Stamp Duty and Registration Fees: These are government levies and are crucial for the legal validation of your property purchase.

Goods and Services Tax (GST): Applicable on under-construction properties.

Brokerage Fees: If you engage a real estate broker, their fees need to be factored in.

Maintenance and Upkeep: Consider the cost of maintenance, repairs, and renovation, which could be recurrent or one-time expenses.

Home Loan Related Charges: Include processing fees, prepayment charges, and interest payments if you are availing a home loan.

Legal Fees: This includes fees for legal consultation, property title verification, and other legal formalities.

Other Miscellaneous Expenses:

Costs like society membership charges, utility connection charges, etc.

Understanding and planning for all these financial aspects will provide a clear picture and ensure that your real estate investment in India is well within your financial means.

This meticulous financial planning is paramount to making a sound and rewarding investment, aligning with both your short-term and long-term financial objectives.

Finding the Right Property

Investing in real estate, especially as an NRI, requires a diligent approach to finding the right property. This phase involves researching, shortlisting, and leveraging both online and offline resources to zero in on a suitable property. Here’s a detailed breakdown of the process:

Researching and Shortlisting Localities:

Market Research:

Familiarize yourself with the real estate market trends in different regions.

Look into the appreciation rates, rental yields, and infrastructure development in prospective localities.

Locality Analysis:

Consider the proximity to essential amenities like schools, hospitals, shopping complexes, and public transportation.

Check the safety, cleanliness, and the overall environment of the locality.

Future Developments:

Research on upcoming infrastructure projects or commercial developments that might enhance the property value in the future.

Neighbourhood Comparisons:

Compare different localities on parameters like price, amenities, and future growth prospects to shortlist the most suitable ones.

Getting a Real Estate Advisor:

The right advisor is not just a guide but a partner in your real estate journey, ensuring every decision made is informed, every opportunity explored is viable, and every step taken is in the right direction towards fulfilling your property aspirations.” – Raja Shambhu, Chairman, Creative Proptech

Finding a Reliable Real Estate Advisor:

Look for experienced and reputable real estate Real Estate Advisors who have a good understanding of the market and the legal framework.

Communication:

Establish clear communication channels with the agent, ensuring they understand your preferences, budget, and other requirements.

Property Viewing:

Arrange for property viewings either virtually or through trusted contacts in India.

Negotiation:

Utilize the expertise of the Real Estate Advisor to negotiate the price and terms with the seller.

Online Portals and Listings:

Exploration:

Explore online real estate portals to browse through listings, compare prices, and read reviews.

Virtual Tours:

Many portals offer virtual tours of properties, which are invaluable for NRIs to get a better sense of the property.

Online Forums and Communities:

Join online real estate forums and communities to gain insights from other buyers and investors.

Document Verification:

Some portals provide document verification services to ensure the legal standing of the property.

Funding Your Investment

The financial blueprint of your real estate investment in India largely hinges on the funding route you choose. Funding options range from self-funding to availing home loans. Here’s an in-depth look at these alternatives and the steps involved:

Self-funding

Savings:

Utilizing your savings is the most straightforward way to fund your property investment.

Ensure that this does not deplete your emergency funds or compromise your financial stability.

Liquidation of Assets:

Liquidating existing assets like shares, mutual funds, or other properties to generate the necessary funds.

Retirement Accounts and Fixed Deposits:

Cashing in on retirement accounts or fixed deposits, although it’s crucial to understand the tax implications and penalties involved.

Home Loans and Financing in India

Exploring Lenders:

Research and compare various banks and financial institutions offering home loans to NRIs.

Look for competitive interest rates, favorable repayment terms, and minimal processing fees.

Loan Application:

Submit a loan application with the necessary documentation.

The lender will assess your creditworthiness, loan repayment capacity, and the property’s legality before sanctioning the loan.

Loan Disbursement:

Upon approval, the loan amount is disbursed, either in full or in installments, directly to the seller or the developer.

Loan Eligibility and Documentation

Eligibility Criteria:

Typically includes a good credit score, stable income, age, and the property’s legal status.

Required Documentation:

Identification proof, income proof, tax returns, credit score report, property documents, and other relevant documents as per the lender’s checklist.

Legal Clearance:

Ensure that the property has clear legal titles, with no encumbrances, to satisfy the lender’s due diligence process.

Loan Agreement:

Carefully review the loan agreement, understanding the terms, interest rates, and the repayment schedule before signing.

The funding avenue you choose significantly impacts your financial portfolio, so it’s essential to weigh the pros and cons associated with each option. If opting for a home loan, ensure that you meet the eligibility criteria and have all the necessary documentation in place for a smooth application process. Whichever route you choose, it should align with your financial goals, ensuring a secure and rewarding real estate investment in India.

Due Diligence

Executing due diligence is a crucial step in the real estate investment process, especially for NRIs. It involves a thorough examination and verification of the legal, procedural, and regulatory aspects of the property and the project. Here’s a detailed guide on how to conduct due diligence:

Verifying the Legal Status of the Property:

Encumbrance Certificate:

Obtain the encumbrance certificate to check for any legal dues or complaints against the property.

Land Use Verification:

Verify the zoning and land use regulations to ensure that the property complies with local municipal laws.

Building Approval Plan:

Check the building approval plan to ensure that the construction is approved by the local municipal authority.

Checking the Title and Ownership:

Title Deed Verification:

Examine the title deeds to ensure the seller has the clear title and ownership of the property.

It’s advisable to trace the title history for at least the last 30 years.

Legal Assistance:

Engage a lawyer to conduct a thorough title verification and provide a legal opinion on the property’s title.

Ownership Verification:

Ensure that the seller is the rightful owner, and there are no disputes or litigations concerning the property.

RERA Registration of the Project:

RERA Verification:

Verify that the project is registered under the Real Estate (Regulation and Development) Act (RERA), which provides a layer of protection to buyers.

Checking RERA Website:

Visit the RERA website of the respective state to check the project details, developer’s credentials, and any grievances filed against the project.

Project Status:

Review the project status, completion timelines, and compare it with the commitments made in the sales agreement.

Developer’s Track Record:

Look into the developer’s past projects, delivery timelines, and any pending or past legal issues.

Due diligence is the cornerstone of a risk-averse real estate investment. It sheds light on the legal and procedural sanctity of the property, ensuring that your investment is secure and compliant with all requisite regulations. This meticulous examination, although time-consuming, can save you from potential legal hassles and financial losses in the long run. It’s advisable to engage legal and real estate professionals to ensure a thorough due diligence process, paving the way for a smooth and hassle-free investment experience.

Making the Purchase

After thorough due diligence and securing the necessary funds, the next step in your real estate investment journey is making the actual purchase. This phase encompasses drafting agreements, making payments, and registering the property in your name. Here’s a detailed breakdown of this crucial stage:

Drafting and Signing the Agreement to Sell

Drafting the Agreement:

Have a legal expert draft the Agreement to Sell, which should detail the transaction terms, including the sale amount, payment schedule, and the date of transfer of property.

Ensure that it mentions any liabilities, encumbrances, or any other material facts concerning the property.

Reviewing the Agreement:

Thoroughly review the agreement to ensure all terms and conditions are as per the discussions.

Seek clarifications and make amendments if necessary, to ensure complete transparency and understanding between the parties involved.

Signing the Agreement:

Once satisfied with the terms, both parties should sign the agreement in the presence of witnesses.

It’s advisable to get the agreement notarized for additional legal sanctity.

Making the Initial Payment

Payment Schedule:

Abide by the payment schedule outlined in the agreement.

Typically, an initial token amount is paid at the time of signing the agreement, followed by a more substantial down payment.

Receipts and Acknowledgments:

Obtain signed receipts for all payments made.

Keep a meticulous record of all financial transactions related to the property purchase.

Registration of the Property

Preparation for Registration:

Prepare the final Sale Deed with the help of a legal expert, ensuring it adheres to the terms outlined in the Agreement to Sell.

Submission of Documents:

Submit the Sale Deed along with other necessary documents to the local sub-registrar office for registration.

Payment of Stamp Duty and Registration Fees:

Pay the applicable stamp duty and registration fees, which are usually a percentage of the property’s sale value.

Completion of Registration:

Upon verification, the sub-registrar will register the Sale Deed, making you the legal owner of the property.

Collect the registered documents and keep them safely.

Updating Land Records:

Ensure that the land records are updated with your name as the new owner, which may require a visit to the local municipal authority.

Making the purchase is a meticulous process that requires careful attention to legal and procedural details. Engaging legal and real estate experts can significantly streamline the process, ensuring that your property purchase abides by all legal and regulatory requisites. This careful approach not only secures your investment but also sets the stage for a hassle-free ownership experience.

Property Management

Post-acquisition, the management of your property is crucial, especially for NRIs who may not be physically present to oversee the day-to-day affairs. Effective property management ensures that your investment remains secure, profitable, and well-maintained. Here’s a closer look at the aspects involved:

Hiring a Property Manager:

Finding a Reliable Manager:

Look for experienced, reputable property managers or management firms with a good track record in the locality of your property.

Roles and Responsibilities:

Define the scope of their services, which may include rent collection, maintenance, handling tenant issues, and ensuring statutory compliance.

Fee Structure:

Understand their fee structure, which could be a monthly fee or a percentage of the rental income.

Regular Updates:

Establish a system for regular updates and reports on your property’s condition, tenancy, and any other pertinent issues.

Renting Out Your Property:

Setting the Right Rent:

Research local rental rates, consider the amenities offered, and set a competitive rent to attract and retain tenants.

Tenant Screening:

Conduct thorough background checks on prospective tenants to ensure they are reliable and will maintain your property well.

Rental Agreement:

Draft a clear and comprehensive rental agreement outlining the terms of tenancy, rent amount, maintenance charges, and other conditions.

Regular Inspections:

Conduct, or have your property manager conduct, regular inspections to ensure the property is being well-maintained.

Maintenance and Upkeep:

Routine Maintenance:

Schedule regular maintenance checks to catch and fix issues before they escalate, be it plumbing, electrical, or structural concerns.

Repair Works:

Promptly attend to necessary repairs to keep the property in good condition and ensure tenant satisfaction.

Cleanliness:

Ensure the property is cleaned regularly, and common areas are well-maintained.

Compliance:

Ensure compliance with local laws and regulations concerning property maintenance and safety.

Property management is a long-term, ongoing commitment that requires a hands-on approach to ensure your investment continues to appreciate and yield returns. Engaging professional help and leveraging technology for remote monitoring can significantly ease the management burden on NRIs. Ensuring a well-maintained property not only enhances its value but also contributes to a satisfying and profitable real estate investment experience in India.

Frequently Asked Questions (FAQs) on NRI Investment in Real Estate in India

1. Can NRIs buy agricultural land in India?

No, NRIs are not allowed to buy agricultural land, plantation property, or farmhouses in India. However, they can inherit such properties.

2. How can NRIs transfer funds for buying property in India?

NRIs can transfer funds through normal banking channels or through the funds in their NRE (Non-Resident External), NRO (Non-Resident Ordinary), or FCNR (Foreign Currency Non-Resident) accounts maintained in India.

3. Are there any restrictions on the number of properties NRIs can own in India?

There is no restriction on the number of residential or commercial properties that NRIs can own in India.

4. Can NRIs avail of home loans in India?

Yes, NRIs can avail of home loans from Indian banks and financial institutions. However, the loan tenure, interest rates, and other terms may vary from those offered to resident Indians.

5. Is Power of Attorney necessary for NRIs buying property in India?

Given that NRIs might not be physically present in India during the property purchase process, granting Power of Attorney (PoA) to a trusted relative or friend in India can facilitate a smoother transaction.

6. What are the tax implications for NRIs on the sale of property in India?

NRIs are subject to Capital Gains Tax on the sale of property in India. The tax rate and exemptions might vary based on the duration of property ownership and other factors.

7. Can NRIs repatriate the proceeds from the sale of property in India?

Yes, NRIs can repatriate the proceeds from the sale of property in India, subject to certain conditions and approvals from RBI. It’s advisable to consult with a legal or financial advisor to understand the procedures and limitations.

8. How do NRIs determine the fair market value of the property they intend to purchase?

It’s advisable for NRIs to consult with reputable real estate advisors, engage in market research, and use online property valuation tools to determine the fair market value of the property.

9. Can NRIs rent out their properties in India?

Yes, NRIs can rent out their properties in India. The rental income can be credited to their NRO, NRE, or FCNR accounts.

10. What happens if an NRI becomes a resident of India after purchasing a property?

The properties owned by an NRI before becoming a resident of India remain unaffected. They can continue to own, hold, transfer or dispose of the property as per the regulations applicable to NRIs.